Economic nexus — state by state guide

This post has been updated for 2026 economic nexus thresholds and state rules.

Economic nexus means an out-of-state seller may be required to register, collect, and remit sales tax in a state once it exceeds that state’s sales threshold, even if it doesn’t have a physical presence in the state. In most states, this threshold is $100,000 in sales, though some states also apply transaction-based rules or higher revenue thresholds.

Here are the 2026 economic nexus thresholds for all U.S. states plus the District of Columbia and Puerto Rico.

| State | Economic nexus threshold | Transaction rule | Includable sales | Marketplace sales included | Measurement period |

|---|---|---|---|---|---|

| Alabama | $250,000 | None | Retail sales | Excluded | Previous calendar year |

| Alaska | $100,000 | None: Repealed 2025 | Gross sales | Included | Current or previous calendar year |

| Arizona | $100,000 | None | Gross sales | Excluded | Current or previous calendar year |

| Arkansas | $100,000 | Or 200 transactions | Taxable sales | Excluded | Current or previous calendar year |

| California | $500,000 | None | Gross sales (TPP only) | Included | Current or previous calendar year |

| Colorado | $100,000 | None: Repealed 2019 | Retail sales | Excluded | Current or previous calendar year |

| Connecticut | $100,000 | And 200 transactions | Gross receipts (retail sales of property + services) | Included | 12-month period ending Sep 30 |

| Delaware | No sales tax | None | N/A | N/A | N/A |

| District of Columbia | $100,000 | Or 200 transactions | Retail sales | Included | Current or previous calendar year |

| Florida | $100,000 | None | Taxable sales | Excluded | Previous calendar year |

| Georgia | $100,000 | Or 200 transactions | Gross sales (TPP only) | Excluded | Current or previous calendar year |

| Hawaii | $100,000 | Or 200 transactions | Gross sales | Included | Current or previous calendar year |

| Idaho | $100,000 | None | Gross sales | Included | Current or previous calendar year |

| Illinois | $100,000 | None: Repealed 2026 | Retail sales | Excluded | 12-month period |

| Indiana | $100,000 | None: Repealed 2024 | Gross sales | Excluded | Current or previous calendar year |

| Iowa | $100,000 | None | Gross sales | Included | Current or previous calendar year |

| Kansas | $100,000 | None | Gross sales | Included | Current or previous calendar year |

| Kentucky | $100,000 | Or 200 transactions | Gross sales | Included | Current or previous calendar year |

| Louisiana | $100,000 | None: Repealed 2023 | Retail sales | Excluded | Current or previous calendar year |

| Maine | $100,000 | None: Repealed 2022 | Gross sales | Excluded | Current or previous calendar year |

| Maryland | $100,000 | Or 200 transactions | Gross sales | Included | Current or previous calendar year |

| Massachusetts | $100,000 | None | Gross sales | Excluded | Current or previous calendar year |

| Michigan | $100,000 | Or 200 transactions | Gross sales | Included | Previous calendar year |

| Minnesota | $100,000 | Or 200 transactions | Retail sales | Included | 12-month period |

| Mississippi | $250,000 | None | Gross sales | Excluded | 12-month period |

| Missouri | $100,000 | None | Gross sales (TPP only) | Included | 12-month period |

| Montana | No sales tax | None | N/A | N/A | N/A |

| Nebraska | $100,000 | Or 200 transactions | Retail sales | Included | Current or previous calendar year |

| Nevada | $100,000 | Or 200 transactions | Retail sales | Included | Current or previous calendar year |

| New Hampshire | No sales tax | None | N/A | N/A | N/A |

| New Jersey | $100,000 | Or 200 transactions | Gross sales | Included | Current or previous calendar year |

| New Mexico | $100,000 | None | Taxable sales | Excluded | Previous calendar year |

| New York | $500,000 | And 100 transactions | Gross receipts | Included | Previous four sales tax quarters |

| North Carolina | $100,000 | None: Repealed 2024 | Gross sales | Included | Current or previous calendar year |

| North Dakota | $100,000 | None | Taxable sales | Excluded | Current or previous calendar year |

| Ohio | $100,000 | Or 200 transactions | Retail sales | Included | Current or previous calendar year |

| Oklahoma | $100,000 | None | Taxable sales | Excluded | Current or previous calendar year |

| Oregon | No sales tax | None | N/A | N/A | N/A |

| Puerto Rico | $100,000 | Or 200 transactions | Gross sales | Excluded | Seller's accounting year |

| Rhode Island | $100,000 | Or 200 transactions | Gross sales | Included | Previous calendar year |

| South Carolina | $100,000 | None | Gross sales | Included | Current or previous calendar year |

| South Dakota | $100,000 | None | Gross revenue | Included | Current or previous calendar year |

| Tennessee | $100,000 | None | Retail sales | Excluded | 12-month period |

| Texas | $500,000 | None | Gross revenue | Included | 12-month period |

| Utah | $100,000 | None: Repealed 2025 | Gross sales | Excluded | Current or previous calendar year |

| Vermont | $100,000 | Or 200 transactions | Gross sales | Included | 12-month period |

| Virginia | $100,000 | Or 200 transactions | Retail sales | Excluded | Current or previous calendar year |

| Washington | $100,000 | None: Repealed 2019 | Gross sales | Included | Current or previous calendar year |

| West Virginia | $100,000 | Or 200 transactions | Gross sales | Included | Current or previous calendar year |

| Wisconsin | $100,000 | None: Repealed 2021 | Gross sales | Included | Current or previous calendar year |

| Wyoming | $100,000 | None: Repealed 2024 | Gross sales | Excluded | Current or previous calendar year |

2025-2026 updates to economic nexus threshold rules

States continue to simplify economic nexus rules by moving away from transaction-based thresholds and relying primarily on revenue thresholds. Below are the confirmed changes to economic nexus thresholds affecting remote sellers in 2025 and 2026.

- Alaska (effective January 1, 2025): Repealed the 200-transaction threshold. Economic nexus is now based solely on $100,000 in gross sales. [1]

- Utah (effective July 1, 2025): Eliminated its 200-transaction threshold, leaving $100,000 in sales as the only economic nexus trigger. [2]

- Illinois (effective January 1, 2026): Removed its 200-transaction threshold. Remote sellers now establish economic nexus once they exceed $100,000 in gross receipts. [3][4]

These changes reduce the likelihood that low-dollar, high-volume sellers trigger economic nexus based on transaction count alone.

For a broader view of how sales tax rules are evolving beyond nexus thresholds, see our overviews of sales tax changes in 2025 and sales tax changes in 2026.

![]()

How economic nexus works

Economic nexus rules vary by state. Differences include what sales count toward the threshold, whether marketplace sales are included, and how the measurement period is calculated. Because of this, a business may trigger nexus in one state while remaining below the threshold in another.

Economic nexus most commonly affects:

- Ecommerce businesses selling through their own websites

- Sellers operating on marketplaces like Amazon or Ebay

- SaaS companies and subscription businesses selling digital goods or remote services

Once a business exceeds a state’s threshold, most states require registration and tax collection to begin immediately or in the following period. That’s why ongoing nexus monitoring matters, especially for businesses selling across multiple states.

South Dakota v. Wayfair, Inc. established economic nexus in 2018

In 2018, the U.S. Supreme Court’s decision in South Dakota v. Wayfair, Inc. allowed states to require out-of-state sellers to collect sales tax based on economic activity, not just physical presence. Since then, states have adopted and refined economic nexus thresholds, with many updating or repealing transaction-based rules as ecommerce continues to evolve.

How do you know when you’ve triggered economic nexus in a state?

To determine whether you’ve triggered economic nexus, you need to track your sales in each state using that state’s rules, not just your own reports. Simply adding up sales by state often isn’t enough, because states apply different inclusion rules when determining nexus.

What trips sellers up is that states calculate nexus differently. For example:

- Some states count gross sales, including exempt transactions

- Others count only taxable sales

- Many states require marketplace sales to be included, even if the marketplace collects tax

- Measurement periods vary, including calendar year and rolling 12-month reviews

When you sell in multiple states, these differences make manual tracking risky. It’s easy to cross a threshold without realizing it, or delay registration because your numbers don’t line up with how a state defines nexus.

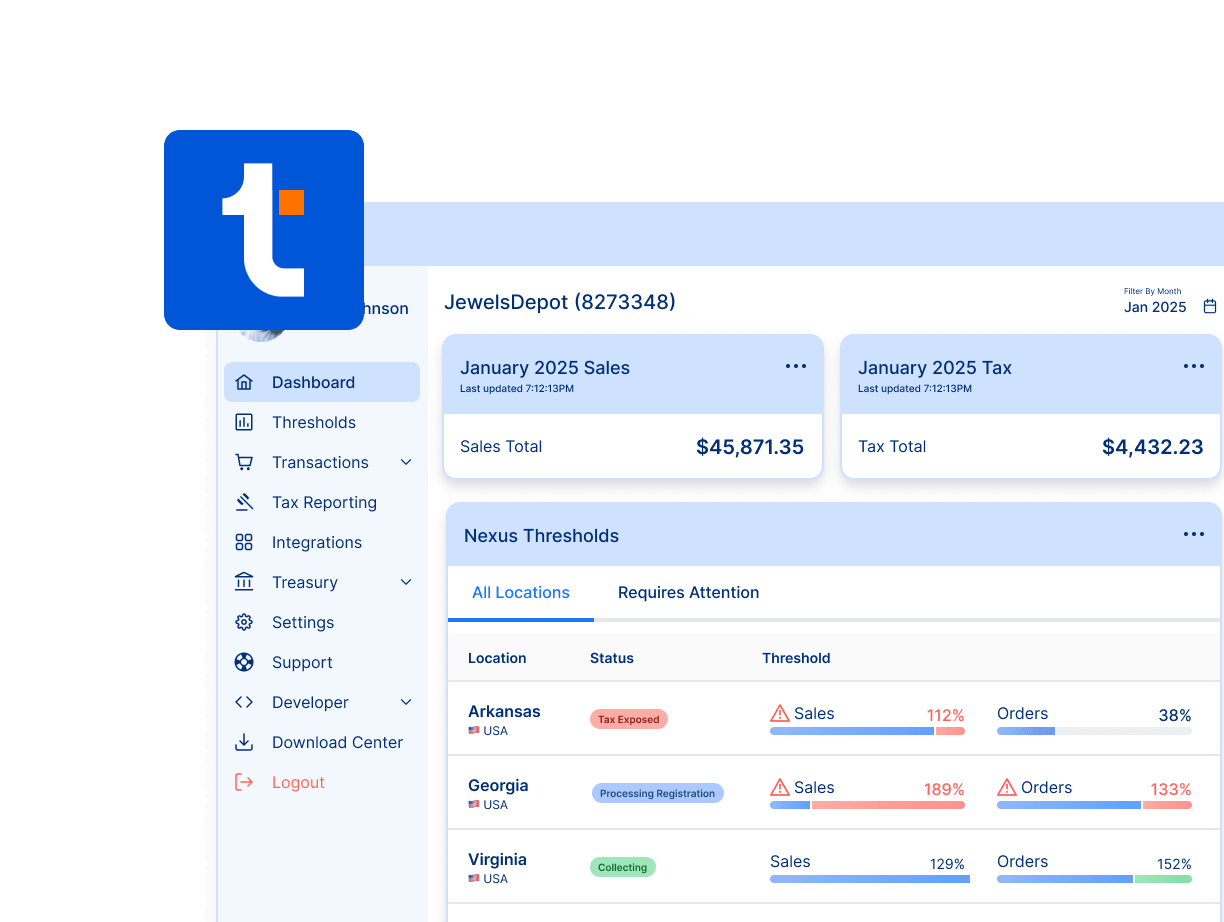

TaxCloud removes that guesswork with economic nexus tracking

It tracks your sales against each state’s economic nexus rules, alerts you when you’re approaching a threshold, and supports multi-state sales tax registration once nexus is triggered. Whether you sell through your own site or a marketplace, TaxCloud applies the correct inclusion rules in the background and handles sales tax filing and remittance so you stay compliant everywhere you sell.

What to do after you cross a sales tax nexus threshold

Once you cross a state’s economic nexus threshold, you’re required to register, collect, and remit sales tax in that state. When those obligations begin depends on the state. Some require action immediately, while others allow registration at the start of the next filing period or year.

Although the exact process varies by state, the steps generally follow the same pattern:

- Register for sales tax. You typically register online through the state’s tax authority. This requires basic business information, such as your legal entity details, contact information, and banking information.

- Start collecting sales tax. After registration, you must begin charging sales tax on taxable sales made into that state.

- File and remit sales tax. Filing frequency varies by state and seller volume. Some businesses file monthly, while others file quarterly or annually. You can find 2026 sales tax due dates for every state here.

Because these timelines differ by state, it’s easy to miss a registration deadline or start collecting too late, especially when you sell into multiple states.

Not sure where you stand with economic nexus?

Economic nexus rules vary by state and are easy to misinterpret. A quick conversation can help you sanity-check your business’s exposure and see how TaxCloud’s nexus tracking works in practice.

Economic nexus obligations when selling through a marketplace

Many businesses sell through both their own ecommerce site and online marketplaces like Amazon or Etsy. In most states (but not all), marketplace sales count toward your economic nexus threshold, just like sales made through your own store.

In some states, marketplaces are required to collect and remit sales tax on behalf of sellers. Even in those cases, your marketplace sales may still count toward your nexus threshold. That means you can trigger nexus in a state even if you aren’t responsible for collecting tax on those marketplace transactions yourself.

Examples of states where the marketplace may collect and remit sales tax for you include:

- Alabama

- Illinois

- New Jersey

- Oklahoma

- Pennsylvania

- Tennessee

- Texas

- Utah

- Virginia

- Wisconsin

Marketplace rules vary by state, platform, and product type. It’s important to confirm whether your marketplace is collecting and remitting tax on your behalf and whether you still need to register once nexus is triggered.

Failing to register when required, even if the marketplace is collecting tax, can still lead to penalties.

Other types of sales tax nexus to be aware of

Economic nexus is only one way a business can establish sales tax obligations in a state. Even if you don’t meet a state’s economic threshold, other activities can still trigger nexus via physical, affiliate, and click-through nexus.

- Physical Nexus. A business establishes physical nexus by having a physical presence in the state, such as an office, warehouse, or remote employee located in the state, or by storing inventory, attending a trade show, or having an employee travel into the state for work.

- Affiliate Nexus applies when a business has a relationship with in-state entities that promote the business or maintain its market, which includes affiliates, subsidiaries, and companies with shared branding.

- Click-Through Nexus can be triggered when a business pays commissions or referral fees to websites or partners that drive sales within the state.

These nexus types are assessed separately from economic nexus and can apply even at low sales volumes. Sellers with multi-state operations should consider all potential nexus triggers.

Unexpected ways businesses trigger physical nexus

Physical nexus can catch sellers off guard because it’s easy to trigger without realizing it, even when economic nexus thresholds haven’t been met.

Examples include:

- Remote employees or traveling staff. Having employees working or traveling in a state can create a physical connection.

- Trade shows and in-person events. Attending events or making in-state sales, even temporarily, may trigger nexus in certain states.

- Affiliate relationships. In some states, in-state affiliates or referral partners can establish nexus.

- Inventory or fulfillment centers. Storing inventory in a state, including through third-party fulfillment providers, can trigger nexus even if you don’t own the warehouse.

These triggers are assessed separately from economic nexus and vary by state. To learn more about less obvious nexus risks, see our guide to unexpected sales tax nexus triggers.

Catch economic nexus exposure before it becomes a problem

Tracking economic nexus across multiple states is difficult because thresholds, measurement periods, and inclusion rules vary. Many sellers don’t realize they’ve crossed a threshold until after registration should have happened.

TaxCloud monitors your sales against each state’s economic nexus rules and alerts you when you’re approaching a threshold. That gives you time to register, adjust collection, and stay compliant before issues arise. When it’s time to file and remit, TaxCloud helps you keep track of due dates across every state you sell into.

Sources:

-

1.

The Alaska Remote Seller Sales Tax Commission (ARSSTC) Clinton Singletary, Statewide Municipal Sales Tax Director. Re: Uniform Code Amendments – August 2024. Source link

- 2.

-

3.

The Illinois General Assembly by the Legislative Information System Bill Status of HB2755 - 104th General Assembly. Source link

-

4.

The Illinois General Assembly by the Legislative Information System Public Act 104-0006. HB2755 Enrolled. Source link