What is physical nexus? A guide for ecommerce and multi-state sellers

Written by

VP of GTM

Published

A physical nexus is the legal connection between a business and a state. It is established when businesses develop a physical presence within state lines.

That nexus makes the business responsible for collecting a sales tax on any transaction made within the state’s borders.

Qualifying physical nexus triggering activities include everything from office spaces to warehouses. Even remote employee or contractor activity can serve as a nexus point.

While the inventory itself is not taxed, the nexus does give the state authority. From that point, taxes are collected on a transaction-by-transaction basis on sales in the state.

It’s common for ecommerce businesses and 3PL warehouses to develop physical nexuses that they don’t even know about. This often results in penalties and back tax obligations that can sneak up on unsuspecting businesses.

What triggers the physical presence nexus?

Physical nexus triggering activities occur any time a “tangible” connection has been made between a business and a state.

There are six common trigger categories, many of which come as a surprise to growing businesses.

A physical office, store, or location

Physical offices, storefronts, or warehousing/showroom locations are, arguably, the most obvious physical nexus points. That said, many businesses are still surprised by how minor the connection point can be.

Even a single leased desk in a shared office space counts as a physical nexus.

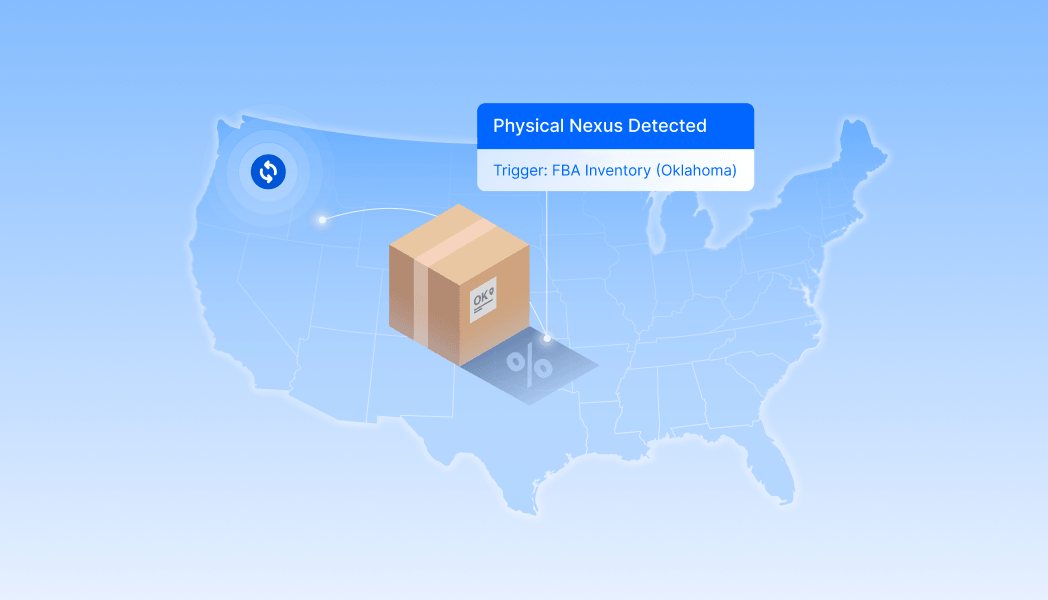

Inventory stored in the state

Inventory storage within state boundaries qualifies as a physical nexus trigger. In the case of self-leased warehouses, this connection is at least straightforward. However, subtler nexus-triggering activities include:

- Products held in Amazon FBA fulfillment centers.

- Third-party logistics warehouses, including ShipBob, Red Stag, and more.

- Consignment locations.

It does not matter if you do not own the warehouse and have never been there. More than 20 states have confirmed that simply storing inventory in a third-party warehouse is enough to create a physical nexus.

That said, recent legal precedents have pushed back on this standard. In 2022, a court case found that Pennsylvania could not force out-of-state FBA sellers to collect sales tax purely based on Amazon-stored inventory. [1]

To this point, however, the Pennsylvania ruling is an outlier.

Employees in the state (including remote workers)

Any W-2 employee working in a state — even if only part-time and remotely — creates a physical nexus. This was established by the Supreme Court case Standard Pressed Steel v. Washington. [2]

The remote-work boom of the 2020s has created thousands of accidental nexus points for businesses all over the country. This means that if you hire a Triple-A coder who works from her family room in Ohio, you most likely are creating an inadvertent nexus.

Remote work activity also triggers an income tax nexus that requires payroll tax obligations alongside unemployment insurance registration requirements.

Contractors, sales reps, and agents

Depending on the nature and frequency of a contractor’s work, even 1099 activity can create a physical nexus.

Traveling sales reps can also establish the connection.

Trade show attendance and temporary presence

Trade show attendance has been determined to qualify as a physical nexus in approximately twenty states. This is particularly true in cases where transactions are being made at the event.

That said, many of these states will offer “safe harbor” thresholds that evaluate connection points based on the level of activity taking place. For example:

- California: Up to 15 days of trade show activity per 12-month period AND under $100,000 in trade show income [3]

- Illinois: No more than 2 trade shows per calendar year, no more than 8 total days, under $10,000 in receipts [4]

- Tennessee: Up to 20 days per calendar year of trade show presence [5]

- Ohio: Up to 7 nexus-creating activities per year and under $25,000 in gross sales [6]

States that do not publish safe harbor guidelines typically treat any trade show activity as being nexus-triggering.

Many businesses are surprised by how stringently trade-show-related nexus events are enforced. New Jersey is famously aggressive when it comes to enforcement, requiring registration 15 days before any retail sale can be made at a trade show.

Auditors across all fifty states may carefully review exhibitor lists and activity levels to identify nexus-triggering activity.

Affiliate, click-through, and drop shipping arrangements

In-state affiliate, subsidiary, or referral partnerships that result in sales can trigger physical nexus in some states. Click-through nexus categories can include the payment of in-state bloggers, influencers, or website owners who collect a commission for in-state sales.

Dropshipping-related nexus activity can be complicated. Businesses selling products shipped by an in-state supplier do not automatically inherit nexus status. However, in-state transactions can still create complicated tax obligations.

A simple example of physical nexus requirements in action

To illustrate the point, here is a hypothetical scenario that could trigger a physical nexus:

A WooCommerce brand operating in Texas sells skincare products. ShipBob stores their inventory in warehouses located in Pennsylvania and Nevada. When the Pennsylvania warehouse receives the product, a physical nexus is immediately established for the skincare business within the state. The same is true for Nevada.

Because of this, the business is now responsible for registering for a sales tax permit in both states and collecting the appropriate sales tax on any order shipped to a Pennsylvania or Nevada customer. They will then need to file returns based on each state’s schedule and remit the collected tax.

These requirements are not applicable to transactions made outside of Pennsylvania or Nevada, but apply only to in-state customers.

The tricky thing is that these requirements apply to any state where inventory is stored. Consequently, an FBA seller can easily wind up with nexus obligations in 15 states.

Common scenarios that create unexpected physical nexus

Many physical nexus connections come as a surprise to growing businesses that did not realize they’d developed a “tangible” connection with states where they are not actively operating.

Below are nexus triggering events that often catch companies off guard.

Amazon FBA inventory

Amazon distributes inventory across a national network of warehouses. Distribution decisions are based on demand-related forecasting. FBA sellers have no control over where their inventory is held.

Consequently, FBA sellers will routinely have 10-15 nexus connections that they knew nothing about.

All states that collect a sales tax now require Amazon to collect and remit taxes on marketplace sales. [7] FBA sellers may still need to:

- Register for sales tax permits in nexus states (some states require this even when Amazon collects)

- File “zero returns” showing what Amazon collected

- Collect their own sales tax on any non-Amazon sales to those states (Shopify, their own website, wholesale, Walmart Marketplace, etc.)

- Address potential income tax, franchise tax, or property tax obligations triggered by inventory presence (California has actively pursued these)

All other Amazon FBA sales tax nexus requirements are met by the platform.

Third-party logistics (3PL) warehouses

A 3PL, or third-party fulfillment provider, picks, packs, and ships orders for ecommerce sellers. The physical nexus point created in 3PL sales tax situations is similar to that of FBA. However, there are important differences.

Unlike Amazon, 3PLs are not classified as marketplace facilitators. This means that the seller is fully responsible for collecting, filing, and remitting sales taxes in every state where their inventory is held.

Remote employees

Remote employees living in a different state from their employer create a physical nexus in their location. During the pandemic, many businesses accidentally created multiple nexus points when they allowed employees to relocate.

This is a common occurrence for SaaS companies, as well as other businesses with heavily distributed teams.

Trade shows and temporary in-state activity

We described earlier how some states have safe harbor rules that allow limited trade show activity without physical nexus risk.

States that lack these laws are often very stringent about nexus enforcement. In some states, even product samples are enough to trigger a physical nexus.

Physical nexus laws vs. economic nexus

| Physical nexus | Economic nexus | |

|---|---|---|

| What creates it | Tangible presence in the state (inventory, employees, office, trade show, etc.) | Sales volume into the state crossing a dollar or transaction threshold |

| Origin | Long-standing standard, predates Wayfair | Established by the 2018 South Dakota v. Wayfair Supreme Court decision |

| Typical threshold | No threshold — even one employee or one unit of inventory can trigger it | Typically $100,000 in sales OR 200 transactions per year (varies by state) |

| How it's tracked | Internal awareness of where your people, inventory, and operations are located | Sales reports broken down by state |

| When obligations start | Immediately upon physical presence | Upon crossing the threshold (sometimes the following calendar period) |

| Common triggers | FBA inventory, 3PL warehouses, remote employees, trade shows | Crossing $100K+ in sales to a state without physical presence |

To complicate things further, businesses can have a physical nexus, economic nexus, both, or neither, in any state in the country. Either nexus triggers a sales tax obligation in that state, though physical nexus generally takes legal precedence. If you have it, you will owe, regardless of sales volume.

What to do if you’ve triggered physical sales tax nexus

If you’ve triggered a physical nexus, there are five clear steps to take.

Step 1: Identify every state where you have physical nexus

Begin by inventorying your physical presence. This audit should include:

- Office locations

- Employee home addresses

- Contractor work locations

- FBA/3PL warehousing locations

- Trade show activity in the past year

If you are an FBA seller, you will be able to pull inventory location reports from Seller Central.

Once you have completed your review, cross-reference the information with each state’s physical nexus rules.

TaxCloud helps automate much of this work.

Step 2: Register for sales tax permits in each nexus state

You’ll next need to complete each state’s registration process before you can legally collect physical nexus sales tax.

Some states will require this registration even when Amazon or another marketplace facilitator is collecting tax on your behalf.

Step 3: Set up collection on your sales channels

Next, set up your ecommerce platform so that you can collect the correct sales tax rate for each state, county, and city.

Local rates can vary, sometimes quite significantly, within a single state. Illinois has hundreds of taxing jurisdictions.

Marketplace facilitator sales (Amazon, Etsy, Walmart, eBay) are typically handled by the platform, but direct-channel sales are the seller’s responsibility.

Step 4: File returns on each state’s schedule

Each state sets its own filing frequency requirements. These can vary from monthly to annually, depending on local guidelines and your sales volume.

Many states require “zero returns” even when no tax was collected during the period. A missed return can trigger a late filing penalty even if no tax is owed.

Step 5: Consider back-tax exposure and voluntary disclosure

You may be liable for back-tax exposure if your physical nexus existed without detection in prior periods. Most states offer Voluntary Disclosure Agreements (VDAs) that allow businesses to come forward, settle prior liability, and often reduce or waive penalties.

SST (Streamlined Sales Tax) program

24 states participate in the Streamlined Sales Tax (SST) program, a system designed to simplify multi-state compliance requirements.

Businesses that have a physical nexus in SST states can file through a Certified Service Provider (CSP). The states involved will then subsidize a portion of the filing work. TaxCloud is one of the few CSPs able to reduce compliance costs for businesses dealing with nexus in SST states.

How TaxCloud helps businesses manage physical nexus

TaxCloud tracks nexus obligations across all fifty states. Not only will it notify businesses when they cross physical or economic thresholds, but it will also handle mult-state registration. This means that business owners won’t have to navigate fifty different state portals.

TaxCloud can:

- Calculate correct tax rates at the state, county, and local level for every transaction

- File returns and remits collected tax to each state on the required schedule

- Reduce compliance costs for businesses with nexus in SST member states

Physical nexus — FAQs

Yes. Storing inventory in a state — whether in your own warehouse, a 3PL facility, or an Amazon FBA fulfillment center — creates physical nexus in that state. This applies in nearly every state that imposes sales tax.

Yes, FBA nexus can occur. When Amazon stores your inventory in a fulfillment center, you have physical nexus in that state. However, because of marketplace facilitator laws, Amazon collects and remits sales tax on Amazon marketplace sales — though you may still need to register and may owe tax on non-Amazon sales, plus potentially income or property tax.

Yes. A single remote employee working from a state — even part-time, even from their home — generally creates physical nexus in that state for sales tax purposes. The same applies to many independent contractors.

It depends on the state. About 20 states treat trade show attendance as a nexus trigger, especially if sales or orders are taken at the event.

Many states offer safe harbor exemptions for limited attendance — California allows up to 15 days, Illinois allows 2 shows and 8 days, and others vary.

Physical nexus is created by tangible presence in a state (inventory, employees, office, etc.).

Economic nexus is created by sales volume into a state, typically $100,000 in sales or 200 transactions per year.

A business can have one, both, or neither in any given state.

Generally no. If you sell a product that’s drop-shipped by a supplier from their warehouse, the supplier’s presence doesn’t transfer to you. Your nexus is determined by your own physical presence, not your supplier’s location.

Often yes. Many states require sellers with physical nexus (such as FBA inventory) to register for sales tax even when Amazon is collecting on the seller’s behalf. Some states also require filing zero-dollar returns showing the marketplace-collected tax.

Yes — and it’s extremely common. Most FBA sellers, 3PL users, and companies with remote employees have physical nexus in multiple states without realizing it. This is the most common compliance gap among growing ecommerce businesses.

You may face back taxes, late filing penalties, and interest in each state where you should have registered. Most states offer Voluntary Disclosure Agreement (VDA) programs that allow businesses to come forward and resolve prior liability with reduced penalties.

Sources:

-

1.

The Commonwealth Court of Pennsylvania Non-Pennsylvania businesses that sell merchandise through Amazon’s FBA Program must collect and remit Pennsylvania sales tax pursuant. Source link

-

2.

The Supreme Court of the United States Standard Pressed Steel Co. v. Department of Revenue, 419 U.S. 560 (1975). Source link

-

3.

The California Department of Tax and Fee Administration (CDTFA) Out-of-State Sellers: Do You Need to Register with California? (Publication 77). Source link

-

4.

Cornell University insignia Cornell Law School Ill. Admin. Code tit. 86, § 150.802 - Trade Show Appearances. Source link

-

5.

The Tennessee Department of Revenue SUT-5 - Activities that Give Out-of-State Dealers Nexus in Tennessee. Source link

-

6.

The Legislative Service Commission and Legislative Information Systems Chapter 5741 | Use Tax; Storage Tax. Source link

-

7.

Amazon Customer Service documentation Tax, Regulatory Fees, and Tax Exemptions. Marketplace Tax Collection. Source link