What is a VDA (Voluntary Disclosure Agreement) and should you get one?

Written by

Kristina Cassone-Rhodes, JD, LL.M

State and Local Tax Attorney and Voluntary Disclosure Agreement Expert

Reviewed by

Cameron McCoolUpdated

Key takeaways

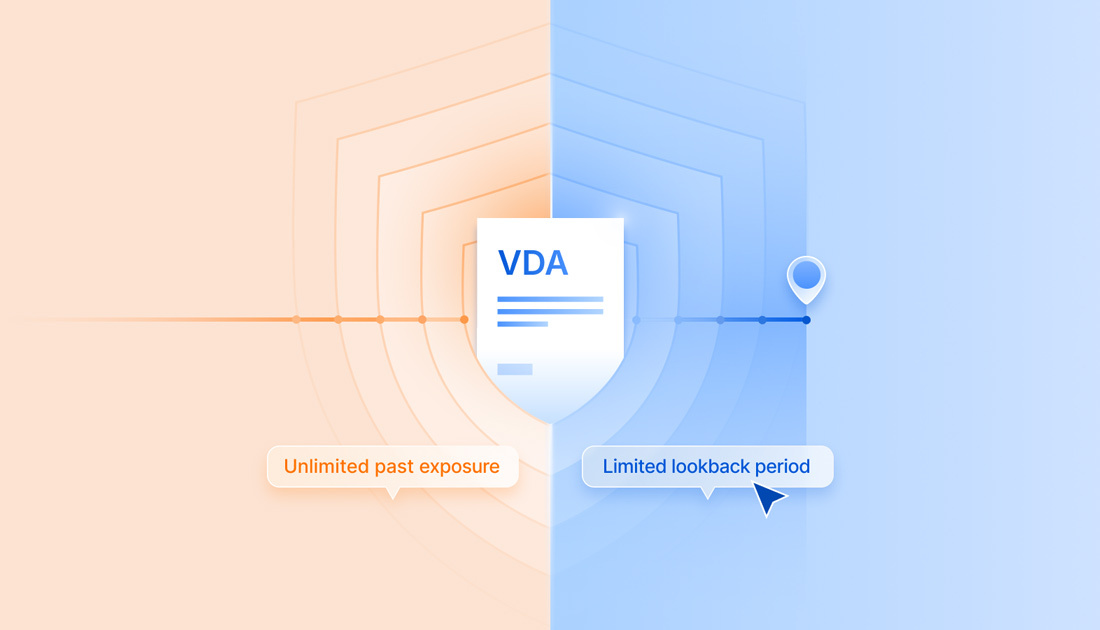

- A VDA lets you fix past sales tax exposure with a limited lookback period and no penalties.

- You only qualify for a VDA if you apply before the state reaches out for audit.

- A VDA specialist can sequence the process correctly and reduce the risk of overpaying or disclosing unnecessary years.

What is a voluntary disclosure agreement?

A voluntary disclosure agreement, or VDA, is a formal agreement between a business and a state tax authority. It allows a business to voluntarily disclose past sales and use tax obligations to become compliant — without facing the full consequences of an audit and unlimited lookback periods.

In most states, a VDA offers three core benefits:

- A limited lookback period (generally three to four years)

- Penalty abatement

- Audit protection for earlier years

VDAs are not loopholes and they do not erase tax liability. They are state-supported programs designed to help businesses correct issues proactively before the state initiates contact.

VDAs can apply to multiple tax types, including sales tax, use tax, income tax, franchise tax, and gross receipts tax. Most exposure begins with sales tax.

Validate your VDA eligibility before the state contacts you

TaxCloud can review your nexus, confirm your exposure window, and advise whether a VDA is the right path.

The benefits of a VDA for sellers

A VDA is usually the most efficient way to fix past sales tax exposure without taking on the full cost of an audit. When I recommend a VDA, it’s because the business has already created a multi-year liability and needs a controlled way to resolve it. A VDA turns a large, undefined liability into something predictable and manageable.

Here’s what a VDA actually solves for sellers:

- It limits how far back the state can look. Without a VDA, a state can often audit as far back as the date nexus began — sometimes five, eight, or even ten years. A VDA usually caps this at three or four.

- It removes penalties. You still owe the outstanding tax and interest, but penalty abatement can make a meaningful difference, especially when liability spans several years.

- It protects earlier years from audit. Once a VDA is underway, most states cannot audit periods outside the agreed lookback. This can be a big win.

- It gives you a defined path to get compliant. Instead of guessing what to file first or trying to unwind years of missed filings alone, the VDA provides a step-by-step timeline with clear requirements.

Businesses don’t use a VDA to avoid responsibility — they use it to avoid chaos. It brings the liability into a manageable window and resolves it before the state reaches out and removes the option entirely.

How sales tax exposure builds — and why states offer VDAs as a solution

States offer voluntary disclosure agreements for a simple reason: businesses fall out of compliance all the time, usually by accident. Sales tax rules differ in every state, thresholds change without warning, and it’s easy for a business to create nexus long before anyone notices.

A VDA gives both sides a structured way to fix the problem. Win-win, in a sense.

The state gets accurate filings and revenue. The business gets a limited lookback period and penalty relief. Everyone avoids a drawn-out audit reaching back a decade.

That matters because sales tax problems rarely show up for businesses as a single dramatic event. They build slowly and quietly.

Here’s where most businesses get caught:

- Expanding into new states without realizing economic nexus was triggered

- Misunderstanding how each state measures thresholds

- Assuming a product is non-taxable everywhere because it isn’t taxable at home

- Relying on marketplace facilitators without understanding which states count marketplace sales toward nexus

- Triggering physical nexus through trade shows, contractors, remote employees, or stored inventory

- Changes in taxability rules (especially for SaaS and digital services)

- Filing income tax in a state but not realizing sales tax is a separate obligation

A VDA exists to clean up these issues in a predictable, controlled window — generally three to four years — while avoiding the cost, uncertainty, and time burden of a full audit.

So when do you need a VDA?

You usually need a VDA when you realize you’ve had taxable sales in a state where you had nexus but weren’t fully compliant. That can mean you never registered at all, or that you registered but left earlier periods unfiled or misreported. Once that exposure stretches across multiple years, a VDA is often the most predictable way to resolve it before the state reaches out.

In my work as a VDA and sales tax consultant, these are the most common situations that create VDA-level exposure.

| Trigger | Why it matters | Risk if ignored |

|---|---|---|

| Economic nexus crossed quietly | Thresholds can be exceeded without realizing it (e.g., $100,000 in sales or 200 transactions). | VAT/GST frameworks don’t map cleanly to U.S. nexus laws. |

| Marketplace sales counted toward nexus | About half of states include marketplace sales when calculating nexus. | Underreporting nexus and remaining unregistered in states where you owe tax. |

| Physical presence you didn’t recognize as nexus | Trade shows, contractors, remote employees, or stored inventory can all trigger nexus. | Immediate registration obligation and exposure starting the day physical presence began. |

| Taxability mistakes | Products taxable in one state may be exempt in another and vice versa; SaaS varies widely. | Multi-year liability from misclassified sales. |

| Income tax filings without sales tax filings | Departments do not communicate; businesses assume one filing covers both. | Surprise audit leading to discovery of unfiled sales tax obligations. |

| International seller misunderstanding U.S. rules | VAT/GST frameworks don’t map cleanly to U.S. nexus laws. | Multi-year unnoticed nexus, often discovered only after first audit contact. |

If any of this sounds familiar, it’s worth evaluating whether a VDA is the right path. The key is to act before the state contacts you. Once there’s any communication from the state, some benefits may no longer be available.

When you don’t need a VDA

Not every exposure requires a VDA. In fact, there are situations where a VDA adds unnecessary time, cost, or paperwork. When I review a client’s data, these are the cases where I usually tell them, “You don’t need a VDA for this.”

- Your exposure is less than one year. If you only have a few unfiled sales tax returns, it’s usually faster to simply file those returns, pay the penalties, and request a penalty abatement. A VDA is designed for multi-year exposure. Anything under a year is normally too small to justify the process. One example I see often: A business that crossed economic nexus in October and realized it by March. That’s a simple back-filing situation, not a VDA.

- The tax due is extremely low. Some states won’t process a VDA at all if the total tax due is below a small threshold (for example, under $500). In those cases, the state usually prefers you file and pay directly. I typically see this when half a business’s sales are wholesale, the rest are exempt, and the actual taxable amount ends up being minimal once we do the analysis.

- Your sales are fully exempt. If a business only makes wholesale sales, government sales, or sells exempt products, there may be no tax liability to disclose. Filing zero returns is usually enough.

- You are already registered and have only made a taxability mistake. Some states allow a VDA for amended returns, but many don’t. If the issue is simply that you misclassified something as exempt, it may be more efficient to amend the returns directly rather than initiate a VDA.

- You have already been contacted by the state. Once a state reaches out — whether it’s a nexus questionnaire, a letter, or an audit notice — you are normally no longer eligible for a VDA. At that point, the focus shifts from voluntary disclosure to audit management.

- You misunderstood a rule but don’t actually owe anything. This happens more than people expect. A company thinks, “We’ve been doing this wrong for years,” but when we run the data, we find the sales didn’t cross the threshold, the product wasn’t taxable, or marketplace sales didn’t count toward nexus in that state. In those situations, a VDA isn’t needed because there’s no exposure to disclose.

Do you need a VDA? Take this self-assessment quiz.

Not sure whether you need a VDA or not? This quiz usually gives a quick, clear answer.

Answer yes or no to each question:

- Have you made over $100,000 in revenue or more than 200 transactions in any state where you are not registered for sales tax?

- Do you have employees, contractors, inventory, or any physical presence in a state where you are not registered?

- Are your products or services taxable in the states where you are not registered?

How to interpret your results:

- If you answered “yes” to two or more: It’s worth speaking with a sales tax specialist. A VDA may be the most cost-effective way to resolve your exposure.

- If you answered “yes” to all three: A VDA is likely necessary. The longer you wait, the higher the risk that the state makes contact — which can remove your eligibility entirely.

How to know for sure: work with a VDA expert

The biggest mistake I see is guessing. Businesses either panic and assume they need a VDA, or they assume they don’t need one and wait too long.

A quick nexus study usually answers the question immediately. It’s a simple review of your last few years of sales by state, any physical presence, and the taxability of what you sell. This can be done by a sales tax specialist or VDA consultant, and it gives you a clear picture of whether you actually have exposure — or if a VDA isn’t needed at all.

Should you file a VDA yourself?

You can complete the VDA process on your own, but I rarely recommend it. Performing everything in the correct sequence matters, and it’s easy to make a mistake that increases liability.

Here are the risks I see most often when businesses try to handle the process themselves:

- Registering too early. Some states disqualify you from a VDA if you register before applying.

- Not knowing which states allow anonymous applications. In certain states, anonymity is beneficial for protecting eligibility in case you’re rejected.

- Misunderstanding lookback rules. A three-year lookback in one state might be a six-year lookback somewhere else.

- Marketplace sales. Some states include marketplace sales in nexus calculations. Others do not. Getting this wrong can inflate or understate liability.

- Data errors. Even small inconsistencies in your application, returns, or exposure timeline can delay the process or increase the tax owed.

A few of the businesses who come to me tried to handle it themselves first — usually after registering out of sequence or receiving a notice. Professional support ensures the application, disclosures, registrations, and filings happen in the right order.

When to apply for a VDA: why timing is everything

You must start a VDA application before a state contacts you. Any notice from the state — a nexus questionnaire, a letter, or an audit inquiry — can remove your business’s eligibility. Once eligibility is gone, so are the benefits — limited lookback, waived penalties, and the ability to disclose on your own terms.

The other reason that timing matters is the pace of each application. The VDA process is not fast. Some states respond in a few weeks. Many applications take three to six months. A few can even take longer, especially with larger exposures or industries like SaaS or ecommerce.

Starting early gives you room to work through the steps without pressure. Waiting increases the chance that a state reaches out first, which can close the door on the very relief the VDA is meant to provide.

Sales tax software can prevent the need for VDAs altogether

Most of the VDA cases I handle start the same way: a business didn’t have clear visibility into where it was creating nexus or what sales were taxable. By the time they realized it, the exposure had already built up. This visibility is what prevents multi-year exposure from building quietly in the background.

Tools like TaxCloud help you spot those issues early. They track state-by-state thresholds, surface physical presence triggers, and keep marketplace and non-marketplace sales cleanly separated. That makes it easier to understand when you need to register — and often prevents a multi-year VDA entirely.

And if a VDA is needed, clean data shortens the process and reduces the risk of mistakes that increase what you owe.

Validate your VDA eligibility before the state contacts you

TaxCloud can review your nexus, confirm your exposure window, and advise whether a VDA is the right path.

Voluntary disclosure agreement — FAQs

A VDA is designed to prevent audits of earlier years. States generally cannot audit periods outside the agreed lookback once the process is underway. The VDA department cannot share information with any other department, so applying for the process will not trigger an audit. Further, all states have audit protection after you apply to the program or sign the agreement. Meaning, if an audit letter comes after an application or signature, depending on the state, the audit is void and the VDA is valid.

Yes, most states allow anonymity during the initial application. Your identity is revealed only after the state confirms your eligibility.

The application approval takes from 1 day to 6 months, depending on the state. The entire process, once accepted, takes 2-3 months if no extension is requested.

Some states restrict VDA eligibility if you are already registered for that tax type. Others still allow entry but may limit benefits. A nexus analysis can determine the best path.