Streamlined Sales Tax Leaders Featured in Inaugural TaxCloud Interview Blog

TaxCloud begins today a series of monthly interview blogs with key players and experts in the world of sales and use tax compliance, innovation, and expertise. It is fitting that we start with the top leaders of the Streamlined Sales Tax Governing Board. The 24 Streamlined member states have made major contributions to tax simplification, education, and innovation.

A very notable innovation was the development of certified service providers to make sales tax compliance easy for sellers while maintaining tax policy flexibility for legislatures. We want to thank Senator Ann Rest and Executive Director Craig Johnson for being so generous with their time and insights. We hope these interviews broaden and deepen the understanding of sales and use tax.

Senator Ann Rest of New Hope, Minnesota is currently the DFL Leader of the Senate Taxes Committee, and has served in the Minnesota Senate since 2001. She has served as President Pro Tem, Vice-Chair of the Senate Taxes Committee, and Chair of the Property Taxes Division. She chairs the Financial Audit Subcommittee of the Legislative Audit Commission. Ann served 16 years in the Minnesota House and served two terms as Chair of the House Tax Committee (1993-1997). She is a retired CPA with a master’s degree in Business Taxation from the University of Minnesota and a master’s in public administration from the John F Kennedy School of Government at Harvard University. She is the current president of the Streamline Sales Tax Governing Board.

Craig Johnson, Executive Director of the Streamlined Sales Tax Governing Board since 2013, is the current COO of this 24-state government collaborative organization, which is focused on simplifying and modernizing sales tax administration. He supports and helps lead the work of the Governing Board and its committees.

Craig has a deep background in state sales taxation, having worked at the Wisconsin Department of Revenue for over 20 years, and serving as a representative of Wisconsin on various committees of the Streamlined Sales Tax Project beginning in 2006. He was a Revenue Field Auditor and a Sales and Use Tax Specialist in the Department’s Administration Technical Services Unit. He was also instrumental in drafting the legislation and implementing the necessary changes when Wisconsin conformed its laws to the requirements of the Streamlined Sales and Use Tax Agreement. Craig is a frequent speaker on sales and use tax issues and is a certified public accountant.

Russ: Craig, Senator Rest, thanks for joining us today. The SSUTA Agreement’s fundamental purpose is to simplify and modernize sales and use tax administration in the member states, in order to substantially reduce the burden of tax compliance. The Agreement focuses on sales and use tax administration systems for all sellers and for all types of commerce.

What are some of the most important things the Streamlined states have done to accomplish this purpose?

Senator Rest: The first thing the SST project members did was to partner with business community representatives to identify the complexities of sales and use tax requirements faced by multistate retailers. Next, they systematically worked together to find solutions that worked from both business and states’ perspective. This collaboration really brought the stakeholders together towards one clear goal.

In fact, thanks to several years of hard work by dozens of delegates, major simplifications were made, and the requirements for member states were reset to greatly reduce the burden on sellers, making compliance with sales and use tax laws much easier – and more uniform. As our business partners know from painful experience, every difference in state laws makes compliance harder.

I think the three most significant early achievements were the implementation of the Streamlined Central Registration System, the development of the Certified Service Provider Program (which your company has been part of since 2010), and the liability relief provisions. We also worked to adopt uniform definitions and administrative practices, among other provisions.

Russ: Let’s start with the Central Registration System. Why is that a big deal?

Craig: Before SST, a seller had to separately register in every member state, each one of which had its own requirements and requests for various pieces of information. Some of these individual state applications were (and continue to be) quite lengthy. In addition, many states charged fees just to get registered, so the costs really added up. With SST, a merchant can now register in all 24 member states with one single application, and, more importantly, it’s free to register.

In fact, when we updated our registration system back in 2015, we specifically developed the new Streamlined Sales Tax Registration System (SSTRS) to require as little information as possible. States can gather additional information later if they need to but getting registered in the SST states is about as easy as it can get now.

Russ: How does that translate to someone who is still on the fence about registering and joining the SST program?

Craig: I knew making the registration process quick and easy was important but what I heard from a former state tax administrator now working for a private firm really helped me understand how much we had improved this process. He told me that for one client the firm had spent many hours completing each of the non-member state’s individual sales tax registration applications. He would gather information, think he had it all, only to find the next state wanted something different. Then once he was done, they had to wait for weeks in some cases before they ever heard anything back from the state to know they were in fact registered.

For the Streamlined member states, he registered them through the SSTRS and was done with all 24 states in a matter of minutes, as opposed to hours (or days) and received the registration confirmation from the SSTRS immediately.

Russ: Senator, I’ve heard both you and Craig say many times that the CSP (Certified Service Provider) program is integral to the success of SST and central in helping multi-state sellers comply with the complexities of sales and use tax laws and regulations. In your mind, what are the key aspects of the CSP program that have made it such a success for multistate sellers?

Senator Rest: SST and the CSPs have harnessed technology to make sales tax compliance very straightforward. Craig can give you more details, but the main point is that a seller can easily just turn over its sales and use tax obligations to a third-party provider (CSP) with confidence that its returns and remittances will happen timely and accurately for little or no cost. And they have liability protections as well.

Craig: I tell businesses to think of CSPs as a way to efficiently and inexpensively outsource one of their most complex and difficult chores. They’ve done it for years with outsourcing their payroll processing, and with the CSP program, businesses have an opportunity to outsource state sales tax. One key difference is businesses must pay for all outsourcing of payroll. Because we compensate CSPs for handling the core obligations for multistate sellers, participants can receive CSP services for little or no cost when they fall under the definition of “CSP compensated seller.”

Russ: Craig, can you explain more of the details of how the CSP program actually works?

Craig: The CSPs have developed tax calculation software programs or tax engines that integrate with the seller’s e-commerce ecosystem (shopping cart software, Enterprise Resource Management platforms and other systems). Through this integration the CSP is able to help the seller calculate and collect tax very quickly — and do it with a high degree of accuracy and complexity.

The CSP’s tax engines determine more than just product taxability. They also look at which state and local taxing jurisdictions are entitled to the tax, what the rates are, and ultimately how much tax is due to each jurisdiction. CSPs also demonstrate through test data provided by the SST states that they can accurately calculate, prepare, and file the simplified electronic return with each of our member states. They then instantly (electronically) transmit the required payments.

Russ: How do you choose which companies are accorded the CSP designation? Can anyone apply to become a CSP?

Part of our vetting process of every CSP is through the use of “test decks.” Each state puts together their own set of transactions for the CSP to run through their system. When you think about all of the types of products sold and the number of different state and local taxing jurisdictions, this can involve thousands upon thousands of test transactions. The CSP is not certified until they demonstrate they handle the tax treatment of all these transactions accurately in every member state. We also make sure the CSPs are keeping their systems up to date. We do this by requiring the CSPs to run new test decks for the states every quarter.

CSPs also need to protect personally identifiable information, set up a trust bank account to handle the funds transfers from the sellers to the CSPs and the CSPs to the states, and they must meet key security requirements. The numerous other requirements are spelled out in the Governing Board rules that CSPs must follow and agree to before the Governing Board can enter into a contract with them.

And yes, anyone can apply to be a CSP. The process is very rigorous, however, so only the most qualified and serious applicants stay the course.

Russ: What do you see as some of the greatest benefits to sellers of using a CSP?

Craig: There are several benefits to sellers using a CSP. First, as I already mentioned, CSPs are a way for sellers to outsource nearly all of their sales and use tax reporting obligations. This lets sellers focus on growing their business as opposed to worrying about their sales tax calculation and reporting deadlines and obligations.

Sellers also gain peace of mind. The CSP assumes responsibility and liability for the proper calculation of sales tax and preparing and filing the required returns. Sellers just need to make sure they provide their CSP with accurate details of the transaction – who the buyer is, what product is being sold, the selling price, where the product is being delivered to the customer, and the date of the transaction.

Russ: What about audits?

Craig: CSPs are responsible for handling any audits the member states may conduct as well as notices the states may send to the seller related to the returns filed by the CSP. Sellers know how time-consuming audits can be, and, under the contract the CSPs enter into with Streamlined, the CSPs agree to handle these audits for their CSP-compensated sellers. Of course, the CSPs might occasionally need to go back to a seller for additional documentation or explanations of some transactions, but the states work directly with the CSPs to resolve the audits – not the sellers.

Russ: Senator Rest, what types of benefits do the states receive and why are they willing to compensate CSPs for handling seller’s sales tax obligations:

Senator Rest: All states’ sales tax collections rely heavily on voluntary compliance and the efforts of sellers to properly calculate, collect and remit the tax. As Craig explained, states have much more confidence that the tax determinations being made by sellers who are using a CSP are correct due to the upfront review of the CSPs system and the ongoing testing of these systems. Having this confidence in the CSP systems helps reduce the resources states must commit to enforcement activities. States also know that the CSPs will file their client’s returns electronically and in a timely manner along with the tax payment.

While the SST states want to make things as simple as possible, they also want to make their own choices about tax treatment. The technology provided by CSPs makes both things possible. The Streamlined States recognized that with the growth in e-commerce they needed to find a way to make it easy for sellers, particularly sellers not physically located in their state, to properly collect and remit their taxes.

As an elected official, I also wanted to find ways to make it easier for my constituents to be able to comply with sales tax collection requirements in other states. That way they can grow their businesses and ship their products to other states without having to worry about figuring out all the nuances of other states’ sales tax laws. The CSP program helps accomplish this. It’s easier for sellers to comply because the technology does all the work about determining taxability.

Russ: Can we talk about the liability relief provisions? One of the things that scares sellers the most about the complexities of selling and remitting taxes in multiple states is the concern over liability when the laws are so complicated. How do your liability relief provisions assist taxpayers?

Senator Rest: Russ, one of the great things about Streamlined and the member states that really helps multistate sellers is transparency and states taking ownership of and standing behind the information and guidance they provide to sellers. Craig can provide some additional details, but every member state has to put together a taxability matrix to let sellers know what is and what is not taxable in their state. It doesn’t cover every product, but it covers the great majority of them. The states also have to put together rate and jurisdiction databases that detail the state and local tax rates that apply within their state based on addresses and/or zip codes. Sellers that rely on and follow this information provided by the states to the CSPs are relieved of liability if the state ultimately determines a particular transaction should have been handled differently. Multistate sellers and accounting firms alike really appreciate this aspect of the SST program.

Craig: And I would add that the taxability matrix really expands a seller’s liability protections – and helps ensure the proper tax is calculated. The CSPs, based on information received from their clients, know what types of products are being sold. If a client is selling a type of product that does not fall squarely within a particular category covered by the Streamlined Taxability Matrix, the CSP can put together additional product categories, complete with a description of the types of products included in the category and have that category reviewed and the tax treatment of the category certified by every member state. Once all the member states certify the tax treatment of these additional product categories, sellers can be assured that, if they properly classify their products within one of these certified categories, they will be protected from liability. Sellers only need to categorize or map their individual products once in the CSP’s system. Once the product is mapped, the CSP’s system takes care of applying the appropriate tax to the products classified in each category for all of the member states.

Russ: Senator Rest, Craig, do you think the CSP program is working as intended?

Senator Rest: I do. The CSP program is about more than just the dollars collected and remitted to the states. It is about removing the burden on sellers, particularly multistate sellers, of having to calculate the appropriate tax, prepare and file the required returns and make the required remittances. We want sellers to be able to focus on growing their business and being successful, and the CSP program helps them do just that.

Craig: Oh yes. Since the Wayfair decision, we have seen the number of sellers registered through Streamlined that are using CSPs quadruple. I also want to stress the importance of the accuracy of sales tax collections by sellers using CSPs. As Senator Rest said, the CSP program is not just about the dollars collected – it is also about the accuracy of the collections – and protections it offers the sellers. No seller wants to find themselves in a position where they over collect the taxes due on multiple transactions and face a possible class action lawsuit. At the same time, no seller wants to under collect the tax and face a possible qui tam lawsuit or assessment by a state if they are audited. The CSP program helps provide these protections.

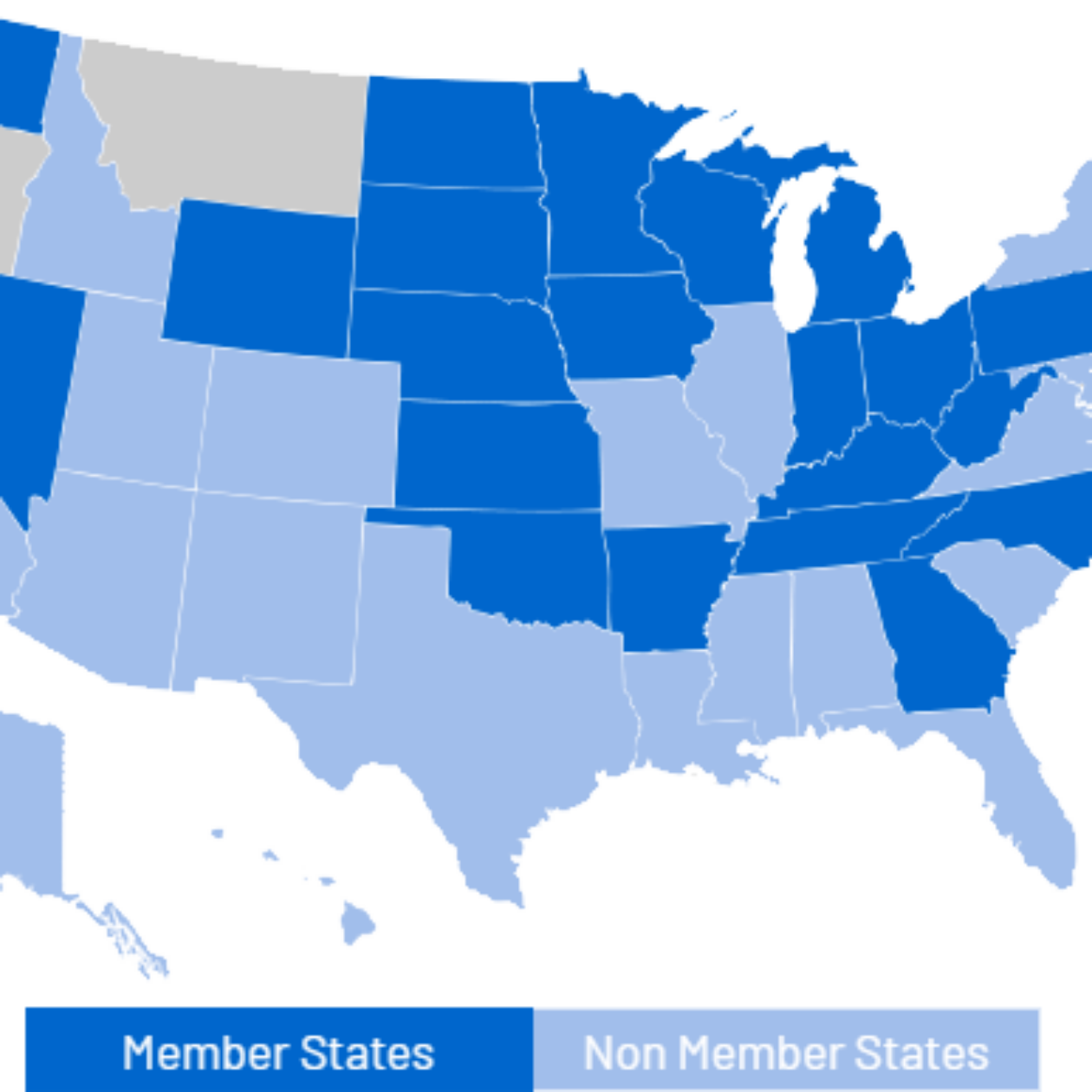

Russ: Currently there are 24 states covered by the contracts between the CSPs and the Streamlined Sales Tax Governing Board. What are you doing to encourage the other states to participate?

Senator Rest: I would like to see every state that imposes a sales and use tax to participate with Streamlined in some manner. About a year and a half ago, we adopted a resolution that allows a nonmember state to participate with the Governing Board if the state adopts some of the most important simplification and uniformity provisions contained in the Streamlined Sales and Use Tax Agreement. We recognize not every state may be able to adopt every requirement contained in the SSUTA, but we also recognize the burdens that sellers face, including my own constituents, making sales into these other states if those states are not doing anything to make it easy for them to comply.

We can continue to reach out to states to encourage them to participate, but we also need those businesses that are adversely affected by a state not participating to reach out to those states and their legislators to explain why their state’s participation is so important.

Craig: Yes, we continue to reach out to the nonmember states to encourage their participation. We point out the benefits that will be realized by both the sellers and the states if the state is willing to make some simplification and uniformity improvements. There’s a real possibility that states failing to make improvements may face legal challenges on their authority to collect from remote sellers because of undue burdens on Interstate Commerce.

We highlight that states can help minimize the risk of such a challenge by doing things such as setting up a rate and jurisdiction database, putting together a taxability matrix, participating in the central registration system, participating in the contracts we have with the CSPs, and providing liability relief to sellers who follow the directions provided by the states.

Russ: What types of things has Streamlined recently completed or is Streamlined currently working on to help sellers comply with the member states’ laws?

Senator Rest: Craig can talk a little bit about some of our more recent specific projects, but as a State Senator, I hear from constituents about the challenges they face not only with respect to sales tax laws but in all aspects of their business and personal lives. I have truly appreciated how the states and business community have been able to sit down together at the table to discuss issues of concern and work cooperatively to find solutions. We have resolved a lot of different issues and will continue to discuss and consider additional issues as time goes on.

Craig: One project we recently completed was the development of numerous disclosed practices related to each of our member state’s remote sales tax collection requirements, marketplace seller requirements and marketplace facilitator requirements.

Since the Wayfair decision, every state with a sales tax has now enacted some type of “economic nexus requirement.” Unfortunately, states are not all uniform in what requirements a seller must meet before they are required to collect and remit a particular state’s sales or use tax, how their thresholds are calculated, etc. The purpose of the disclosed practice is for the states to clearly layout what their requirements are so sellers can easily determine in which states they do or do not have a sales or use tax collection and filing requirement. In fact, Russ, that would be a good future blog.

Russ: Actually, Craig we are already planning to cover that topic in one of our next blogs. Watch this space. What other projects you are working on right now?

Craig: We are working on two projects now of note. One is a project that likely affects every seller and purchaser. We are revising the Streamlined Certificate of Exemption. We want to make it easier for purchasers to understand what they are required to provide to claim certain exemptions in the member states and for sellers to know what they are expected to obtain from purchasers to support the exemption taken and to protect them from potential liability.

Another project relates to the continued growth and evolution of digital transactions. As more and more transactions become strictly digital in nature (i.e., no tangible property is shipped to the customer), sellers only need limited information from a customer to complete the transaction. If only limited information is obtained, this causes challenges for the seller in determining which state and local jurisdictions are entitled to the tax on such transactions. The states and business community are actively working together to determine how to best handle these types of transactions. We work really hard to be responsive to the world of e-commerce as things evolve and understand that a collaborative effort helps make things better and simpler for everyone involved.

Russ: Any last comments you would like to make about Streamlined and the outstanding work being done by your member states in partnership with the business community and CSPs?

Craig: I want to thank you for having this conversation with us. Streamlined has developed into a unique partnership between our member states, the business community and the CSPs, and has resulted in significant benefits to all the parties involved. Sales tax compliance is much easier now in the member states than it was prior to those states adopting the Streamlined requirements. The Streamlined Sales and Use Tax Agreement has really become the gold standard for simplification and uniformity in sales tax administration. But our work is not done. As goods, services, technologies, and selling platforms continue to evolve, we will seek additional opportunities to make sales and use tax compliance as simple as possible.

Join 15,000+ eCommerce owners

Stay informed on sales tax news — sign up for our free newsletter.