Economic nexus explained: How your nexus obligations change as you scale

Written by

VP of Business & Corporate Development

Updated

How economic nexus works

Before you can assess your economic nexus exposure, here’s a refresher on how economic nexus works — what counts toward a threshold, when taxes kick in, and where the rules trip sellers up.

1. Economic nexus thresholds vary by state

Most states use two thresholds or tests. Hit either one and you have nexus in that state:

- $100,000 in annual sales into the state

- 200 transactions into the state

But these thresholds aren’t standardized across all 50 states.

California, Texas, and New York set a higher sales volume test: $500,000 in annual sales. Some states have removed the 200-transaction threshold entirely.

2. Two states require you to hit both tests

Most states require you to exceed the dollar threshold OR the transaction count. Two states require both:

- Connecticut: $100,000 AND 200 transactions

- New York: $500,000 AND more than 100 transactions

A B2B seller with $400,000 in Connecticut sales across 60 large contracts has no economic nexus there, because the transaction threshold isn’t met.

3. Not all revenue counts toward your threshold the same way

$100,000 in California-bound sales triggers economic nexus. That same $100,000 in a state that only counts taxable sales, where most of your revenue is exempt, may not. Two things drive most of this variation: what types of sales count toward your threshold, and whether your marketplace orders are included.

4. Some states count revenue you’re not even taxing

Some states count all revenue toward the threshold, including nontaxable sales, wholesale transactions, and exempt purchases. Others only count retail sales that are subject to tax.

- Counts gross revenue: California, Illinois, Wisconsin

- Counts taxable sales only: Arkansas, Florida, Oklahoma

A B2B seller doing $150,000 in California largely through exempt transactions has nexus there. California counts everything.

5. Marketplace sales count toward your threshold in most states, but not all

In most states, marketplace sales count toward your individual threshold. But not all states follow this rule. Whether marketplace sales count toward your economic nexus threshold or not varies by state, so check every state where you’re selling significant marketplace volume.

In states with marketplace facilitator laws, the platform collects and remits tax on your behalf. But in most states, those sales still count toward your individual threshold.

For the full state chart and breakdown, see economic nexus thresholds by state.

6. The measurement period varies by state

Most states measure your sales and transaction volume against the threshold over the previous or current calendar year.

But a select few use different measurement periods:

- Connecticut: the 12 months ending September 30

- New York: the four immediately preceding sales tax quarters

If you have nexus in a handful of states, tracking these variances manually is manageable. When you expand beyond that, using software that monitors economic nexus automatically is the practical answer.

Economic nexus rules change. Manual tracking doesn't catch it.

Economic nexus rules change without much notice and vary significantly by state. A seller tracking them manually across 10+ states is one update away from a gap. See our breakdown of the best software for tracking economic nexus best software for tracking economic nexus to find the right tool for your stage.

How to manage economic nexus as your operation scales

Managing economic nexus at $200k looks nothing like managing it at $2M. The rules are the same. But the operational problem is vastly different.

Here’s what sellers need to know about economic nexus at every stage of growth: what triggers it, what’s commonly overlooked, and how to manage it without compliance taking up all of your team’s time.

Early-stage sellers ($0–$300k): Triggering economic nexus for the first time

What we see at TaxCloud is that most early-stage sellers learn they’ve triggered economic nexus from a Shopify Tax notification, a CPA flagging it, or a free nexus tool that returns a number they weren’t expecting. And by then, they’ve usually been over an economic nexus threshold for several months or more.

The problem here isn’t compliance complexity or volume. It’s recognition.

What triggers economic nexus for early-stage sellers

Smaller sellers usually trigger economic nexus when sales volume in a single state (usually it’s a home state of the business where it’s started) crosses a threshold.

What early-stage sellers typically overlook

1. Marketplace orders can count toward your threshold in some states, even when the marketplace collects the tax

$70,000 through your Shopify store in Texas + $40,000 through Amazon in the same state = $110,000. Texas includes marketplace sales in your individual threshold. You’ve crossed. Amazon collecting the tax on those orders doesn’t change your nexus status.

2. The obligation started when you crossed, not when you found out

If you crossed an economic nexus threshold in September, the obligation to collect and remit tax on sales in that state started then — the day your sales crossed that threshold in September.

If you’ve been making sales in that state for a while without collecting sales tax from the day you triggered economic nexus, that gap is potential back liability. This situation is quite common and can typically be handled through a Voluntary Disclosure Agreement (VDA).

VDAs exist specifically to help sellers that find themselves in this situation: they cap your lookback period and often waive penalties when you come forward before the state contacts you. The “If you’ve already crossed a threshold” section below covers how to handle it.

3. You don’t owe sales tax on the sales you made before crossing

The revenue you sold into a state before hitting the threshold? You’re not on the hook for sales tax on those. No nexus, no obligation.

What does matter is the sales you made after crossing, in the gap between when you crossed and when you registered and started collecting. That’s where potential back liability lives.

How early-stage sellers manage their economic nexus obligations

At $0–$300k, manually managing nexus is doable. Most sellers here are in one or two states.

What you need in place:

- Sales tracking by state across every channel: your platform’s reporting plus marketplace data pulled separately and combined

- A registration in each state where you’ve crossed, with sales tax collection configured on all channels

- A filing calendar with due dates per state, including zero return deadlines

Pro tip for multi-channel sellers

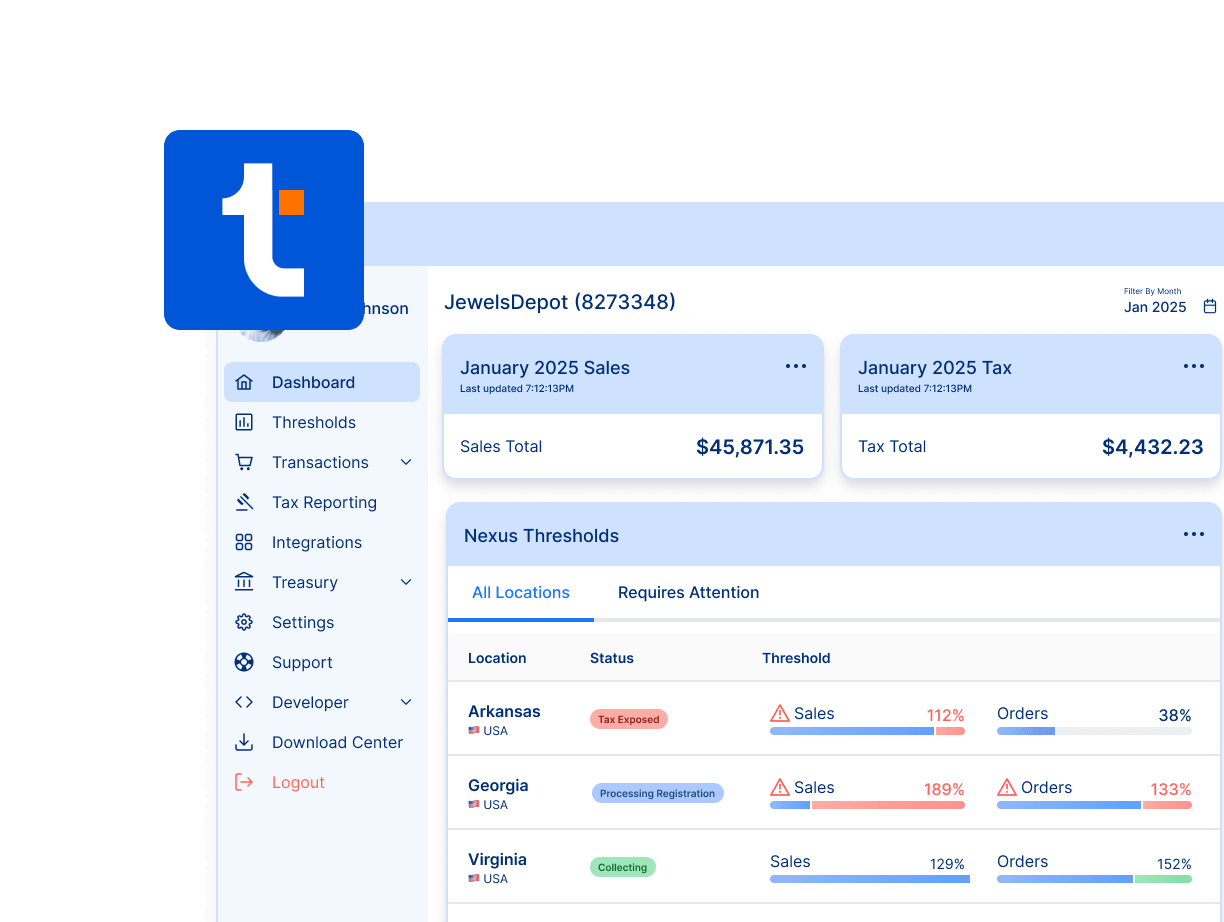

Some platforms only track sales made through their own system. Shopify reports Shopify sales. Amazon reports Amazon sales. If you sell across multiple channels, no single dashboard gives you the full picture — you’ll need to pull data from each and combine it.

TaxCloud’s economic nexus tracking monitors your sales across all channels and alerts you before you cross.

SMB sellers ($300k–$1M): Moving from one nexus state to several

At this stage, you’ve crossed a threshold somewhere and registered. The recognition problem is behind you. The operations problem is starting.

What triggers economic nexus for SMB sellers

The trigger is the same: your sales in a state cross $100,000. But at this stage, it’s happening in more states at the same time. As revenue grows, thresholds in your second and third states start to tip. Each new crossing creates a new registration, a new filing schedule, and new deadlines to track.

Adding a second channel accelerates it. A seller doing $400,000 through their own store plus $200,000 through Amazon has combined state-by-state totals that may already be over threshold in states where neither channel alone looked exposed.

What SMB sellers typically overlook

1. Economic nexus thresholds are different in each state

SMB sellers new to multi-state compliance often assume the threshold is the same everywhere: $100,000 in sales or 200 transactions. It isn’t. California, Texas, and New York set their threshold at $500,000 in sales. Several states have eliminated the 200-transaction threshold entirely. And some states require you to hit both tests to trigger nexus.

2. Not filing zero returns

Once you’re registered in a state, you’re required to file on schedule even in months where you collected no tax. A missed zero return triggers a late filing penalty even when nothing is owed. At two registered states, a missed deadline is manageable. At five, it’s a system problem.

3. Multi-channel data not matching up

Shopify summarizes your Shopify sales. Amazon summarizes your Amazon sales. If you’re selling across both, your combined state-by-state totals don’t live in either report. You need to pull and reconcile both before you can confirm where you stand.

How SMB sellers manage their obligations

At $300k–$1M, manual management can still work, but it needs more structure and oversight.

What you need in place:

- A filing calendar with due dates and frequencies for every registered state, including zero return months

- Multi-channel data pulled and reconciled by state before every filing

- A registration process for new states as you cross thresholds

One provider choice note

You don’t need an enterprise sales tax platform at $300k–$1M. What does matter is choosing a provider who participates in the Streamlined Sales Tax (SST) program as a Certified Service Provider. You won’t see SST savings at this revenue level — but when you scale into mid-market, the savings from free SST filing costs become a real line item. Choosing an SST-eligible certified service provider now means you won’t have to switch later.

TaxCloud handles multi-state registration, filing, and SST enrollment. SST access is included in both Starter and Premium. See how TaxCloud handles multi-state filing.

Mid-market sellers ($1M-$50M): Managing economic nexus across multiple states

At this stage, registering in one or two states feels like the problem is handled. It usually isn’t. At $1M-$50M in revenue, you’re likely crossing new state thresholds every few months.

It happens faster than most mid-market sellers realize, and often in states they weren’t deliberately targeting.

What triggers economic nexus for mid-market sellers

Here, the trigger is the same but it’s happening in more places at once. Revenue crosses thresholds in new states as you grow. New channels accelerate it: if you’ve added Amazon, a wholesale account, or a B2B portal alongside your own store, your state totals are likely higher than any single platform shows. Each channel reports its own sales. Economic nexus counts all of it.

Managing obligations across different jurisdictions, each with its own schedule and rules, is where manual compliance starts to fail.

What mid-market sellers typically overlook

1. Exempt revenue may still count toward your threshold

Some states count all revenue toward the threshold. Others count only taxable sales.

- Gross revenue states: California, Illinois, Wisconsin

- Taxable sales only: Arkansas, Florida, Oklahoma

A B2B seller doing $150,000 in California largely through exempt transactions has nexus there. California counts everything.

2. SST savings — and why provider choice matters now

Access to the Streamlined Sales Tax (SST) program becomes a meaningful cost lever. Eligible businesses file for free in all 24 SST-member states when they work with a Certified Service Provider. At $10-20M+ in revenue, that adds up. More importantly: if you haven’t chosen an SST Certified Service Provider yet, switching later means migration costs and disruption.

TaxCloud is a Certified Service Provider under the SST program. SST access is included in both Starter and Premium plans. For a mid-market business filing in SST-participating states, that’s a meaningful reduction in annual compliance costs compared to non-SST providers.

3. Zero return penalties

Every registered state requires a return on schedule, even in periods with no taxable sales. A missed zero return triggers a penalty even when nothing is owed.

4. Exemption certificate gaps

B2B sellers are responsible for collecting, storing, and renewing exemption certificates state by state. Certificates expire. Missing or expired certificates reclassify exempt sales as taxable during an audit.

5. Filing frequency triggers

Some states move sellers from quarterly to monthly filing once volume crosses a certain level. Miss the trigger and you’re filing on the wrong schedule. Across 15 or 20 states, this compounds quickly.

6. Data reconciliation across all sales channels

At this stage, your sales data lives across multiple systems that don’t talk to each other automatically. Your Shopify store tracks DTC revenue. Amazon Seller Central tracks marketplace orders. QuickBooks logs your books. Stripe captures payment activity. Each platform reports its own version of your revenue, and none of them reconcile automatically against each state’s specific nexus rules.

Before every filing, someone needs to pull data from each source, combine it, and apply the right state-by-state inclusion rules. Done manually, this is time-consuming and error-prone. Done with the right software, it runs in the background.

7. A prior nexus review that only covered economic nexus

Several mid-market businesses have had a formal nexus study done and believe they’re covered. It comes up regularly in our discovery calls: “We had a nexus review done — but it only covered economic nexus, not physical.” Most one-time reviews don’t account for physical nexus at all. If your prior review didn’t look at FBA inventory locations, third-party warehouse arrangements, or remote employee states, it’s likely incomplete.

TaxCloud tip: Don’t overlook physical nexus

If you’re using Amazon FBA, a 3PL, regularly attend conferences or trade shows in other states, or have remote employees, you almost certainly have physical nexus exposure that’s separate from your economic nexus obligations.

Physical presence nexus is a different obligation triggered by presence, not sales volume — it can arise at any stage of growth, not just at scale. See our physical nexus guide to assess your physical nexus exposure.

How mid-market sellers manage multi-state compliance

This is the point where manually managing economic nexus and sales tax compliance starts to break. Filing deadlines multiply. Rules vary by state. The person handling compliance is usually doing it alongside something else.

What needs to be in place:

- Automated tracking across all sales channels, applying each state’s specific rules in real time

- Automated filing on each state’s schedule, with frequency updates when volume triggers a change

- Exemption certificate management: collection, storage, and renewal tracking by state

- SST enrollment through a Certified Service Provider, which eliminates registration fees and filing costs in 24 states

Choose your platform for where you're going, not where you are

At this stage, enterprise sales tax platforms like Avalara, Vertex, and Sovos are often in the conversation. But for US-focused mid-market businesses, these are usually the wrong fit. They’re built for large multi-entity enterprises operating globally.

If you’re a US ecommerce or SaaS business without complex international operations, you’ll pay enterprise pricing for capabilities you’ll never use. The right platform at this stage handles US compliance well, participates in SST, and prices for mid-market scale, not enterprise contracts.

Enterprise sellers ($100M+): Economic nexus complexity at scale

At $100M+ in revenue, you’ve likely already crossed economic nexus thresholds across most US states. Economic nexus is no longer the discovery problem. The question is whether your systems, processes, and compliance teams can keep up.

And for enterprise sellers expanding internationally, the complexity compounds: VAT, GST, customs, and local tax requirements across multiple countries sit alongside US state obligations. That’s a fundamentally different compliance picture from mid-market.

What triggers economic nexus for enterprise sellers

Enterprise sellers are already registered across most states where they do significant volume. Economic nexus is rarely a discovery problem at this scale. The triggers that create new obligations are structural.

Acquisitions bring inherited nexus footprints: each acquired entity has its own registration history, filing obligations, and potentially unresolved exposure. New business lines or subsidiaries may create fresh nexus obligations in states where the parent is already registered but the new entity isn’t. International expansion introduces VAT, GST, and other tax frameworks that sit outside US economic nexus entirely.

What enterprise sellers typically overlook

1. ERP integration gaps

Enterprise operations run through ERPs — SAP, Microsoft Dynamics, NetSuite, Oracle. When sales tax platform data doesn’t reconcile cleanly with ERP records, errors compound at volume. At enterprise scale, small discrepancies across thousands of daily transactions create audit exposure that’s difficult and expensive to unwind.

2. Multi-entity nexus management

Each subsidiary, acquisition, or business unit may have its own nexus footprint, filing requirements, and compliance history. Managing consolidated compliance across entities requires systems that handle independent workflows at the entity level, not just aggregate reporting.

3. Audit trail documentation

Enterprise audits are more extensive and more consequential than mid-market reviews. Every registration, filing, exemption certificate, and rate decision needs a complete, auditable paper trail. Documentation gaps that are manageable at mid-market scale become material liabilities at enterprise scale.

4. Acquisitions create inherited nexus obligations

If you’ve acquired another business, you’ve taken on their nexus footprint, including any states where they owed but never registered. This almost always surfaces during integration or audit. By then, it’s significantly more expensive to resolve.

How enterprise sellers manage compliance at scale

Enterprise compliance requires dedicated infrastructure:

- A dedicated in-house tax function or outsourced tax advisory firm

- Sales tax platforms that integrate natively with SAP, Microsoft Dynamics, NetSuite, and Oracle

- Automated workflows for exemption certificate management, multi-entity filing, and audit support

- Global tax engines where operations extend outside the US

Enterprise platforms like Avalara, Vertex, and Sovos are purpose-built for this level of complexity. For businesses with multi-entity structures, global compliance requirements, or ERP integration dependencies, these platforms are the right fit. The decision should be driven by the complexity of your structure and the scope of your operations — not just revenue.

TaxCloud is built for US ecommerce and SaaS businesses in the small-to-mid-market. If your compliance needs have grown beyond that scope, we’ll tell you.

What to do if you’ve already crossed an economic nexus threshold

Most sellers who discover nexus exposure have been over a state’s threshold for several months. Here’s how to address it.

Step 1: Quantify your exposure

Pull sales data by state for the last 12 months from every channel: your own store, all marketplaces, wholesale, and any other sales channel. Apply each state’s specific rule: gross or taxable sales, marketplace inclusion or exclusion.

Step 2: Decide between VDA and quiet registration

If your exposure is recent (six months or less), register and start collecting going forward.

If your exposure exceeds 12 months, talk to a tax advisor before registering. A Voluntary Disclosure Agreement (VDA) can cap your lookback period (typically three or four years) and waive penalties if you come forward before the state contacts you. VDA services are handled through an external CPA partner and aren’t a TaxCloud service. For significant historical exposure, a VDA is almost always the right path.

Step 3: Register for a sales tax permit in each state where you have nexus

Then configure sales tax collection across every channel you sell through.

Step 4: File on schedule going forward

File returns on each state’s schedule, including zero returns in periods where you collected no tax. Missing a zero return can trigger penalties even when nothing is owed.

The longer you wait, the more expensive this gets. Back taxes compound. Penalties add interest monthly. A VDA window open to you today may close once a state contacts you first.

2025 and 2026 changes to economic nexus thresholds

States have been eliminating the 200-transaction threshold at a steady pace. The pattern is consistent: dollar threshold stays, transaction count goes.

Recent eliminations:

- Alaska: January 1, 2025

- Utah: July 1, 2025

- Illinois: January 1, 2026

- Kentucky: August 1, 2026

Earlier eliminations include Indiana, South Dakota, Wyoming, Louisiana, North Carolina, Maine, and most large states between 2018 and 2021.

If you’ve been tracking nexus using only the transaction count in any of these states, update your approach now.

Not sure where you’ve triggered economic nexus?

A TaxCloud expert can help map your nexus footprint, flag states where you may already have obligations, and point you toward the right next step to get and stay compliant.

Economic nexus — FAQs

Economic nexus is the rule that requires out-of-state sellers to collect and remit sales tax in any state where their sales exceed a threshold, with no physical presence required. Since the Supreme Court’s 2018 decision in South Dakota v. Wayfair, Inc., all 45 states with a statewide sales tax enforce economic nexus laws.

You have economic nexus in a state if your sales activity into that state has crossed the state’s threshold. Most states use $100,000 in annual sales OR 200 transactions over the previous or current calendar year. Marketplace sales count toward your threshold in most states, even when the marketplace collects the tax. If you’ve crossed, you’re required to register, collect, and file.

In most states, yes. Sales through Amazon, Etsy, eBay, and other marketplaces count toward your individual threshold even when the marketplace remits the tax on those orders. However, some states exclude them. Use our economic nexus state by state guide to check which states include and exclude marketplace sales.

Physical nexus is created by a tangible presence in a state: inventory stored there, employees working there, or an office. It has no minimum threshold. Economic nexus is created by sales activity exceeding a state’s dollar or transaction threshold, with no physical presence required. A growing ecommerce business can have both types in the same state at the same time.

Potentially, yes. But it’s more manageable than most sellers expect. Being unregistered doesn’t mean the state is actively tracking every sale you missed. Most states offer Voluntary Disclosure Agreements that allow businesses to come forward, limit the lookback period (typically three or four years), and often waive penalties. If your exposure exceeds 12 months, talk to a tax advisor before registering. Coming forward through a VDA almost always results in a better outcome than waiting for the state to contact you first.

No. Five states have no statewide sales tax: Delaware, Montana, New Hampshire, Oregon, and Alaska. Of these, Alaska is a partial exception: many cities and boroughs impose local sales taxes, and the Alaska Remote Seller Sales Tax Commission administers an economic nexus standard for those jurisdictions.

Yes. TaxCloud monitors your sales against each state’s economic nexus thresholds and sends alerts when you’re approaching a threshold, before you cross it. As a Certified Service Provider under the Streamlined Sales Tax program, TaxCloud handles registration, filing, and remittance across all states, including 24 SST-participating states where eligible businesses file at no cost.

No. If a state has no statewide sales tax, there’s no economic nexus obligation for sales tax purposes. Delaware, Montana, New Hampshire, and Oregon all fall into this category.

Alaska is the exception worth knowing. Alaska has no statewide sales tax, but many Alaskan cities and boroughs impose local sales taxes. The Alaska Remote Seller Sales Tax Commission administers an economic nexus threshold for those local jurisdictions — $100,000 in sales or 200 transactions — which means remote sellers can have collection obligations in Alaskan localities even without any state-level requirement.